New Tax Regime FY 2025-26 (AY 2026-27) — The Deductions and Exemptions Nobody Tells You About

"Most people think switching to the new regime means giving up everything. That's not true — and this guide proves it, point by point"

Every year around March, the same conversation plays out across payroll departments, WhatsApp groups, and CA offices — should I stick with the old regime or go with the new one? And almost always, someone says: "The new regime has no deductions, so if you have investments, stay old."

That's half true at best. Yes, the new regime strips away a long list of deductions — your 80C investments, your home loan interest on self-occupied property, your HRA. But it doesn't strip away everything. There's a fair amount you can still claim, and for a lot of taxpayers — especially those earning between ₹8 lakhs and ₹15 lakhs without massive deduction portfolios — the new regime quietly works out better than they expected.

This guide covers what actually survives. Not what you lose — you've heard that enough. What you can still claim, how it works in practice, and what it means for your tax this year.

First — What Actually Changed for FY 2025-26

Before getting into deductions, a quick orientation on why FY 2025-26 is different from the years before it. The Union Budget 2025 made two changes that together shift the math significantly for middle-income taxpayers:

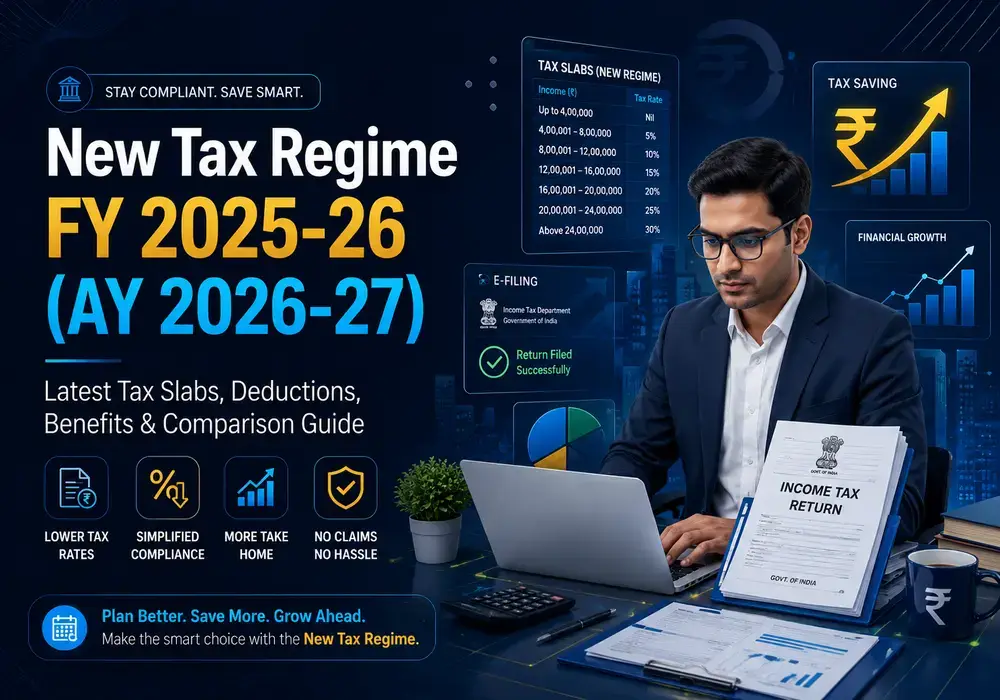

The basic exemption limit under the new regime moved from ₹3 lakhs to ₹4 lakhs. That's a ₹1 lakh increase — small on its own, but it pushes people down into lower brackets and reduces the base amount being taxed.

More importantly, the Section 87A rebate was enhanced. Under the new regime for FY 2025-26, if your total income — after all eligible deductions — doesn't exceed ₹12 lakhs, your entire tax liability is wiped out by the rebate. Zero tax. The slabs still apply technically, but the rebate cancels them entirely up to that ₹12 lakh mark.

And here's the practical magic of this: a salaried person earning ₹12.75 lakhs gross gets the ₹75,000 standard deduction automatically, bringing taxable income to ₹12 lakhs. Tax computes to ₹80,000. Section 87A rebate: ₹80,000. Net payable: zero. That ₹12.75 lakh ceiling for zero-tax isn't accidental — it was designed this way.

The new slab rates above ₹12 lakhs: 15% from ₹12-16 lakhs, 20% from ₹16-20 lakhs, 25% from ₹20-24 lakhs, and 30% above ₹24 lakhs. Significantly lower than the old regime's top slabs for most income bands.

Standard Deduction — ₹75,000, No Questions Asked

This is the one everyone should know and a surprising number of people still don't fully internalise. The standard deduction under the new regime is ₹75,000 for salaried individuals and pensioners — up from ₹50,000 after the Budget 2024 change, and it continues for FY 2025-26.

There's nothing to do for this. No proof to submit. No investment to make. No form to fill. Your employer deducts it automatically when computing TDS, and the income tax portal applies it when you file. It's a flat ₹75,000 off the top of your gross salary before a single slab rate touches it.

For pensioners receiving family pension, the deduction is either one-third of the pension amount or ₹25,000 — whichever is lower. That too continues under the new regime.

Why does this matter? Because it's money you keep without doing anything. And combined with the ₹12 lakh zero-tax zone, it creates that effective ceiling of ₹12.75 lakhs where a salaried employee pays nothing.

Employer's NPS Contribution — Section 80CCD(2)

Here's one that gets far less attention than it deserves. Under Section 80CCD(2), your employer's contribution to your NPS account is deductible from your taxable income — even under the new regime.

The limit for FY 2025-26: up to 14% of basic salary plus DA for both government and private sector employees. This was revised in Budget 2024 — private sector employees previously got only 10%, now they get the same 14% treatment.

The key point here is that this is employer money, not yours. You're not sacrificing take-home pay to get this deduction. If your employer contributes ₹50,000 a year to your NPS as part of your CTC, that ₹50,000 is deductible from your income under the new regime. You didn't pay it — they did — but it reduces your tax.

If your employer isn't already structuring your CTC this way, it's worth raising with HR. A portion of your existing CTC reclassified as employer NPS contribution can reduce your tax meaningfully without costing either party more money. It's one of those restructuring conversations that pays off.

Agniveer Corpus Fund — Section 80CCH

This one is specific and applies to a narrower group, but it's worth mentioning. Under Section 80CCH, amounts received from the Agniveer Corpus Fund by someone enrolled under the Agnipath Scheme are fully deductible. Both the enrollee's contributions and the matching Central Government contribution qualify — and this deduction is available under the new regime.

What it means practically: for Agniveers, the entire corpus payout at the end of the four-year service period is effectively tax-free. This deduction continues for FY 2025-26.

Exemptions That Survive in the New Regime — Several of Them

Deductions aren't the only way taxable income gets reduced. Exemptions — amounts that are never considered income in the first place — also matter, and several of them continue under the new regime. These are the ones worth knowing:

- Leave Encashment on Retirement — Section 10(10AA): if you receive leave encashment when you retire, up to ₹25 lakhs is exempt for non-government employees. The limit was raised from ₹3 lakhs to ₹25 lakhs back in 2023 and this exemption continues under the new regime. If you're anywhere near retirement age, this is a meaningful number

- Gratuity — Section 10(10): gratuity received from your employer remains exempt under the new regime. For government employees it's fully exempt. For private sector employees covered under the Gratuity Act, exemption is the least of actual gratuity, ₹20 lakhs, or 15 days salary per year of service

- VRS Compensation — Section 10(10C): compensation received under a Voluntary Retirement Scheme is exempt up to ₹5 lakhs and this carries forward into the new regime without change

- Life Insurance Policy Proceeds — Section 10(10D): maturity proceeds or death benefits from a life insurance policy continue to be exempt under the new regime, subject to the standard conditions around premium ratios and the ULIP carve-out for annual premiums above ₹2.5 lakhs

- PPF and Sukanya Samriddhi Interest — Sections 10(11) and 10(11A): you can't claim an 80C deduction for contributing to PPF or Sukanya Samriddhi under the new regime, but the interest these accounts earn continues to be completely tax-free. If you have an existing PPF balance earning interest, that interest is still exempt — it doesn't become taxable just because you switched regimes

- Agricultural Income — Section 10(1): if you have genuine agricultural income, it remains exempt under both regimes

- Death-cum-Retirement Gratuity for Government Staff — Section 10(10)(i): fully exempt for Central and State Government employees, local authority employees, and defence personnel. Continues under the new regime

Perquisites and Allowances That Are Still Tax-Free

Beyond formal deductions and exemptions, several things your employer pays you or arranges for you simply don't count as taxable salary — under either regime. These aren't widely discussed but they add up:

- Transport allowance for specially-abled employees: up to ₹3,200 per month is exempt even under the new regime

- Conveyance reimbursement for actual official travel: money paid back to you for travelling on official duty is not taxable. Note — this is a reimbursement against actual expenses, not a flat monthly allowance

- Meal vouchers or office food: meals provided at the office, or non-transferable meal coupons up to ₹50 per meal, are not treated as a taxable perquisite

- Employer's PF contribution: your employer's contribution to your Recognised Provident Fund up to 12% of salary remains exempt. Anything above 12% becomes taxable in your hands

- Tax on perquisites paid by employer: if your employer pays the income tax on a non-monetary perquisite on your behalf, that tax amount is not treated as your additional income

Capital Gains — Same Rules, Both Regimes

People sometimes wonder if the new regime changes how their investment gains are taxed. It doesn't — capital gains have their own tax rates that apply regardless of which regime you're in.

- Long-term capital gains on equity (LTCG): gains on listed equity shares or equity mutual funds above ₹1.25 lakhs are taxed at 12.5% (revised in Budget 2024). This applies under both old and new regimes

- Short-term capital gains on equity (STCG): taxed at 20% under both regimes (revised from 15% in Budget 2024)

- Dividend income: taxed at your applicable slab rates under both regimes — no special treatment

- Section 80TTA — savings account interest: this one is actually lost under the new regime. The ₹10,000 deduction on savings account interest that exists in the old regime is not available under the new one. A small thing, but worth noting

What You Do Give Up — Being Honest About It

For completeness, here's what the new regime doesn't allow, because knowing both sides is how you make the right choice:

- Section 80C: PPF contributions, ELSS, NSC, home loan principal repayment, LIC premiums, SSA contributions — none of these are deductible under the new regime

- HRA — Section 10(13A): if you're paying significant rent and receiving HRA, this exemption is lost. This is the single biggest reason some people in metro cities still benefit from the old regime

- Home loan interest on self-occupied property — Section 24(b): up to ₹2 lakhs deduction is not available under the new regime. If your annual home loan interest is high and your income is moderate, the old regime can win on this alone

- Section 80D — health insurance premiums: not available under the new regime

- Section 80E — education loan interest: not available under the new regime

- Section 80CCD(1B) — additional NPS: your own voluntary contribution of ₹50,000 to NPS is not deductible under the new regime — only the employer's contribution under 80CCD(2) survives

- LTA — Section 10(5): not available under the new regime

So — Which Regime Should You Pick?

Here's the honest version: if your total deductions under the old regime (HRA + 80C + 80D + home loan interest + everything else) add up to less than ₹3.75 lakhs from your gross income, the new regime almost certainly gives you a lower or equal tax bill. The math just works out that way for most middle-income earners.

The old regime wins when: you're paying significant rent in a metro and claiming large HRA, or you have a substantial home loan with interest above ₹2 lakhs, or your overall deduction portfolio genuinely brings your taxable income down by ₹4 lakhs or more from gross. In those cases — run the numbers.

And one thing to remember: if your employer has already deducted TDS under the new regime this year, you're not locked in. At the time of filing your ITR — as long as you don't have business income — you can still opt for the old regime and claim a refund if it works out better. Don't decide under pressure. Calculate first, then file.

FAQs — New Tax Regime for FY 2025-26 (AY 2026-27)

Real questions taxpayers ask — answered without hedging

Q1. My gross salary is ₹13 lakhs — will I pay zero tax under the new regime?

Not quite zero — after the ₹75,000 standard deduction your taxable income is ₹12.25 lakhs, which is ₹25,000 above the rebate threshold, so you'll pay a small tax on that excess at the 15% slab rate.

Q2. I put ₹1.5 lakhs in PPF every year — do I get any deduction for that under the new regime?

No deduction on the contribution — but the interest your PPF earns continues to be completely tax-free regardless of which regime you're in, so your existing PPF balance keeps growing tax-free.

Q3. My company deposits NPS in my name every month — is that deductible even in the new regime?

Yes — employer NPS contributions under Section 80CCD(2) are specifically allowed under the new regime, up to 14% of your basic salary plus DA for FY 2025-26.

Q4. I pay ₹25,000 rent every month in Bengaluru — should I still choose the old regime because of HRA?

Quite possibly yes — with ₹3 lakhs in annual rent in a metro city, your HRA exemption under the old regime could be significant; run a comparison with your actual HRA amount before deciding.

Q5. I retired last year and get a monthly pension of ₹60,000 — what's my tax situation under the new regime?

Your annual pension is ₹7.2 lakhs — after the ₹75,000 standard deduction your taxable income is ₹6.45 lakhs, and the Section 87A rebate brings your tax to zero since it's well under ₹12 lakhs.

Q6. My company already deducted TDS under the new regime but I want to claim HRA — can I switch at filing time?

Yes — if you don't have any business or professional income, you can opt for the old regime when filing your ITR and claim a refund of excess TDS, as long as you file before the July 31st deadline.

Q7. I have a home loan and pay around ₹1.8 lakhs in interest every year — should I worry about giving this up under the new regime?

At ₹1.8 lakhs it's worth comparing carefully — if the new regime's lower slabs save you more than ₹1.8 lakhs times your marginal tax rate, the new regime still wins; if not, stick with the old one.

Q8. I'm taking VRS this year — is my VRS compensation going to be taxed under the new regime?

Up to ₹5 lakhs of VRS compensation is exempt under Section 10(10C) and this exemption continues under the new regime — anything above ₹5 lakhs will be taxed at applicable slab rates.

Q9. I invest ₹50,000 in NPS myself every year for the additional deduction — can I still claim that under the new regime?

No — your own voluntary NPS contribution under Section 80CCD(1B) is not deductible under the new regime; only the employer's NPS contribution under 80CCD(2) is allowed.

Q10. I contribute to my daughter's Sukanya Samriddhi account — the interest is still tax-free, right?

Yes — SSA interest under Section 10(11A) remains completely tax-free under the new regime even though you lose the 80C deduction on the contribution amount itself.

Q11. I sold some equity mutual funds this year and made ₹80,000 in long-term gains — is that taxable?

No — LTCG from equity mutual funds up to ₹1.25 lakhs is exempt, so your ₹80,000 gain falls entirely within the exemption threshold under both old and new regimes.

Q12. My company reimburses my phone and internet bill every month — will that be taxed under the new regime?

No — reimbursements against actual bills for genuine official use are not treated as a taxable perquisite; the key distinction is that it's reimbursement of actual expenses, not a fixed monthly allowance.

Q13. I earn salary from my job and also do freelance work — can I switch between regimes every year?

Only if you drop the freelance income — once you have business or professional income, switching to the old regime is a one-time choice, and if you ever switch back to new, you can't return to old again.

Q14. I haven't told my employer anything about regime preference — what are they using for TDS?

The new regime is the default for FY 2025-26 — your employer will apply it unless you've specifically submitted a declaration asking for the old regime.

Q15. My income is ₹9 lakhs — is there any point in claiming deductions under the old regime or should I just go with the new one?

At ₹9 lakhs under the new regime your taxable income after standard deduction is ₹8.25 lakhs and tax is around ₹42,500 — for the old regime to beat that, your total deductions would need to exceed roughly ₹1.5 to 2 lakhs, which isn't hard if you have PPF, insurance, and 80D; still worth calculating.

Want a personalised comparison for your income and deduction profile? Talk to a CA before filing your ITR for AY 2026-27 — a 30-minute consultation can save you more than the fee.

For more detail about How to File Online ITR Return Filing in India, Call us at +918178508772 or send your query Today! For latest updates follow us on Instagram and facebook.